The National e-Invoicing System (KSeF) in Poland and the new JPK_VAT structure from 1 February 2026

From 1 February 2026, a new version of the Polish VAT reporting structure applies: JPK_V7M(3) for monthly VAT settlements and JPK_V7K(3) for quarterly settlements.

The change applies under Polish tax law and affects all active VAT taxpayers in Poland submitting JPK_VAT files for periods starting from February 2026.

The key practical change is closely linked to the implementation of the National e-Invoicing System (KSeF) in Poland. In the VAT records section of JPK_VAT, taxpayers must now indicate either:

- the KSeF invoice number, or

- the reason for its absence, using one of the new codes: OFF, BFK or DI.

Even though the mandatory use of KSeF is introduced gradually in 2026, the new JPK_VAT structure applies universally, regardless of when a given company becomes subject to mandatory e-invoicing.

For more context on why these changes were introduced, see our earlier post: Draft regulation: new invoice markings in JPK_VAT in connection with KSeF.

In this article:

Who must apply JPK_V7M(3) and JPK_V7K(3) – and from when?

The new JPK_VAT variants must be submitted for the first time for February 2026, within the standard deadline applicable to that settlement period.

This obligation covers both:

- monthly VAT taxpayers (JPK_V7M), and

- quarterly VAT taxpayers (JPK_V7K),

as the VAT records section is still submitted on a monthly basis, even under quarterly settlement rules.

A critical compliance point is that the requirement to report a KSeF number or OFF/BFK/DI is assessed as at the moment of submitting the JPK_VAT file.

In practice, this means that the decisive factor is the status of the document on the filing date, not the transaction date or the invoice issue date.

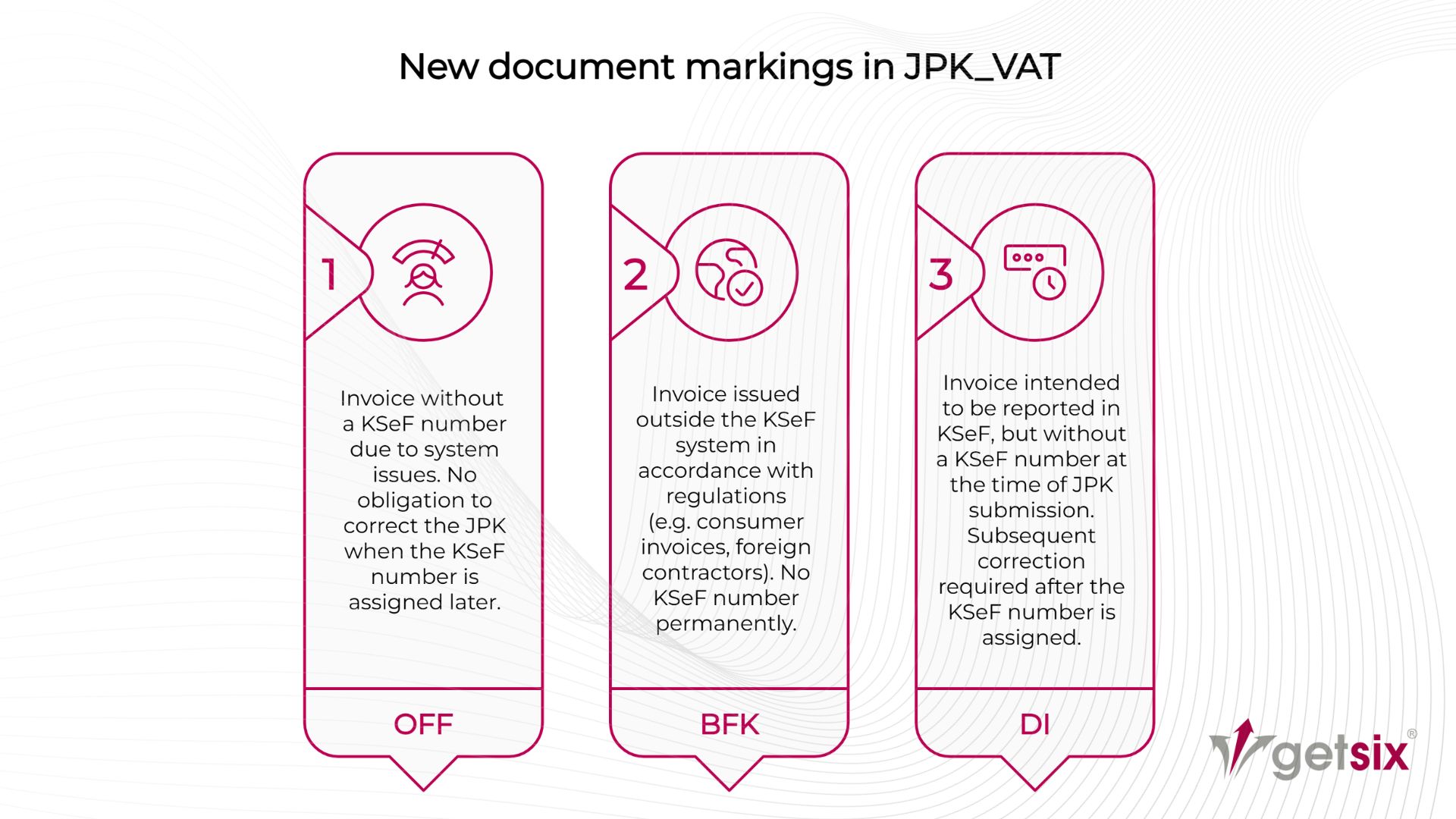

New reporting requirement: KSeF number or OFF, BFK, DI

Under the updated JPK_VAT structure, only one value may be reported per entry. Taxpayers must indicate either the KSeF number or exactly one reason code explaining its absence:

- KSeF number – if the invoice has already been assigned a KSeF number by the filing date,

- OFF – if statutory conditions for this code are met and the invoice does not yet have a KSeF number on the filing date,

- BFK – if the invoice was issued outside KSeF in cases permitted by Polish regulations (e.g. invoices issued to consumers or other transactions excluded from KSeF),

- DI – if the reported document is not an invoice or if the invoice should ultimately be registered in KSeF, but no number is available at the time of filing (including offline24 mode or temporary system unavailability).

From an organisational perspective, this requires companies to define clear and strict internal rules determining:

- when the accounting system should retrieve a KSeF number, and

- when OFF, BFK or DI should be assigned automatically.

OFF, BFK and DI in practice – how to interpret the codes

OFF – invoices affected by KSeF system failures

The OFF code applies where invoices are issued during technical failures on the KSeF side, and no KSeF number is available at the time of JPK_VAT submission.

An important practical consequence is that, as a rule, OFF does not automatically require a JPK_VAT correction solely to supplement the KSeF number if it becomes available later. This distinguishes OFF from DI in terms of follow-up obligations.

BFK – invoices legitimately issued outside KSeF

BFK covers invoices issued outside KSeF in situations explicitly permitted by Polish VAT regulations, such as B2C invoices or other transactions not processed through the Polish e-invoicing system.

For internationally operating companies, BFK is often relevant on the purchase side, where VAT records include documents received from foreign suppliers that are not part of the Polish KSeF framework.

DI – temporary reporting before a KSeF number is assigned

DI is a temporary indicator showing that a document is reported without a KSeF number, even though such a number is expected to be assigned later in the normal course of events.

The key compliance implication is procedural: once the KSeF number becomes available, companies should be prepared to correct the VAT records and replace DI with the KSeF number, if required by the applicable regulations.

Do existing JPK_VAT codes (GTU, RO, WEW, FP, IMP) still apply?

Yes. The new JPK_VAT structure does not eliminate existing markings such as GTU, RO, WEW, FP, TP or IMP. These codes continue to apply alongside the new KSeF-related requirement.

In practice, a single VAT entry may include:

- the relevant transaction-specific codes, and

- either a KSeF number or OFF/BFK/DI.

For example, in VAT settlements related to import of goods (IMP), DI may still apply if no KSeF number is available at the time of filing and the structure requires justification for its absence.

JPK_VAT corrections under the new structure – procedural priorities

From a management and compliance perspective, two areas require particular attention:

1. Status assessment at the filing date

The decision whether to report a KSeF number or OFF/BFK/DI is made at the moment of submitting JPK_VAT. This requires coordination between invoicing teams, accounting and IT systems.

2. Correction mechanics (especially for DI)

Where DI situations occur, companies should clearly define:

- who monitors the assignment of KSeF numbers,

- when and how VAT record corrections are initiated,

- how the use of DI is documented for audit and tax control purposes.

Sanctions – why JPK_VAT changes are not just a technical update

Regardless of ongoing discussions on penalties related directly to KSeF invoicing, JPK_VAT reporting risks remain significant.

If the head of the competent Polish tax office identifies errors in VAT records that prevent proper verification of transactions, the taxpayer will be formally requested to:

- submit a correction within 14 days, or

- provide explanations.

Only if the taxpayer fails to respond on time, responds late, or does not effectively refute the identified errors, may the tax authority impose a financial penalty of PLN 500 per error by administrative decision.

Importantly, sanctions are not automatic and are linked to the correction procedure and the taxpayer’s response.

February 2026 implementation checklist for entrepreneurs – how to reduce risk

The following steps usually deliver the fastest compliance benefits:

- Document and transaction mapping – identify which documents will carry a KSeF number and which require OFF/BFK/DI.

- Decision rules in accounting systems – configure logic for assigning codes and implement controls limiting manual errors.

- KSeF integration and status handling – ensure your system can retrieve and correctly reflect KSeF numbers in VAT records.

- DI correction procedures – define monitoring, responsibilities and correction triggers.

- Team training – short, operational training for accounting and invoicing staff typically reduces errors from the first reporting period.

- Test JPK export – generate a trial JPK_V7M(3) or JPK_V7K(3) using real data and verify consistency before the submission deadline.

For organisations with complex VAT structures, international transactions or fragmented IT systems, a process-based implementation approach is often the most effective way to ensure OFF/BFK/DI rules are aligned with accounting and document workflows from day one.

At getsix®, within our accounting services in Poland, we support businesses in structuring VAT records, defining reporting rules and ensuring that JPK_VAT reporting remains consistent with operational documentation and Polish compliance requirements. Contact us.

Legal basis:

- Regulation of the Minister of Finance and Economy of 12 December 2025 amending the regulation on the detailed scope of data included in VAT tax declarations and VAT records.

If you have any questions regarding this topic or if you are in need for any additional information – please do not hesitate to contact us:

CUSTOMER RELATIONSHIPS DEPARTMENT

ELŻBIETA

NARON-GROCHALSKA

Head of Customer Relationships

Department / Senior Manager

getsix® Group

***